Most biotech M&A coverage correctly highlights where capital is flowing, which therapeutic areas are hot, and which companies are poised to shape the future of medicine. For BD, corporate strategy, or investing, such information is useful. It gives context. It sets benchmarks. And it surfaces the big moves worth watching.

But that’s only part of the story.

The true levers behind M&A activity—factors that determine whether a deal even gets to term sheet—are quiet, structural, and easily overlooked. And if you are making decisions that influence your company’s positioning, assessing potential targets, or crafting your narrative to potential acquirers, these are valuable but possibly not so glamorous.

Here are three trends that aren’t getting much airtime—but they are being followed by forward-thinking acquirers and will likely shape how we think about biotech deal-making today:

1. Platform Companies Are Valued for Optionality, Not Just Assets

What’s changing:

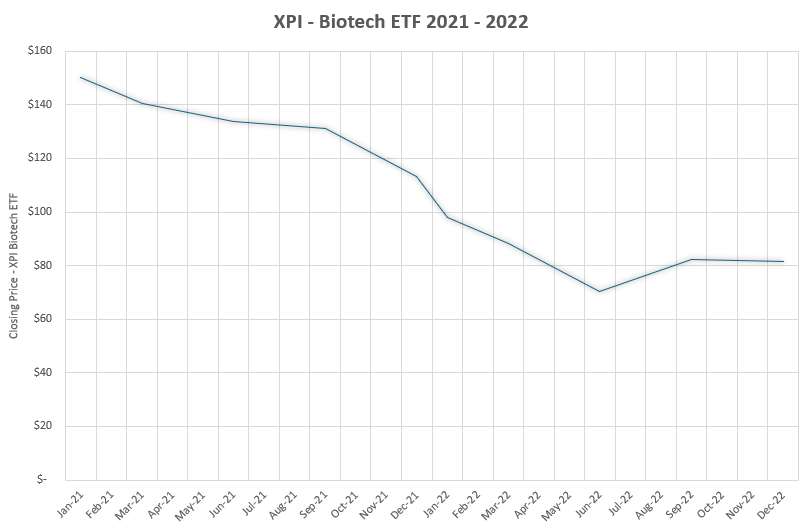

Platform technologies are slowly regaining the favor that they had during the 2022 correction to the 2021 biotech boom (see XBI ETF below). Acquirers are seeking the business flexibility from systems that generate multiple viable assets across indications, once the early biology is validated.

Why it matters:

It is risky to acquire just one molecule—a buyer would prefer momentum. A target’s value proposition is stronger if its platform can serve multiple therapeutic areas (with strong preclinical rationale). The lead asset helps, but the true appeal stems from the replicability of success.

Who did it right: AstraZeneca’s $1B Acquisition of EsoBiotec in March 2025.

EsoBiotec’s specialty: In-vivo CAR-T cell therapies through simple injections rather than the lengthy process of extracting patient T-cells, inserting CAR-encoding genes in a lab, and reinjecting modified T-cells into the patient. This acquisition is expanding AstraZeneca’s ongoing expansion into innovative treatments, which now includes seven cell therapy programs.

2. Manufacturing Strategy Is Now a Front-End Filter

What’s changing:

CDMO relationships and manufacturing readiness used to be buried in diligence checklists. Today, they are moving from nice-to-have to must haves in go/no-go decisions. A promising gene therapy program could get derailed if the acquirer ignores tech transfer risks, capacity bottlenecks, or inflexible CDMO contracts.

Why it matters:

Companies can no longer treat CMC as a backend function, something to sort out after the term sheet. Today’s buyers want crisp, credible operational narratives, not just clinical promise. Execution risk has moved upstream in the valuation checklist.

Who did it right: AstraZeneca’s $2.4B Acquisition of Fusion Pharma in Mar 2024.

Fusion Pharma’s Specialty: Targeted radiotherapy delivers directly to cancer cells while minimizing damage to healthy tissue, making them a promising approach to cancer treatment. In addition to clinical-ready assets, AstraZeneca paid close attention to manufacturing capabilities. Producing radioconjugates involves specialized manufacturing infrastructure and techniques; hence, robust manufacturing and supply chain capabilities are critical to success and were central to the acquisition decision.

3. The Smart Money is in the $100–$500M Range

What’s changing:

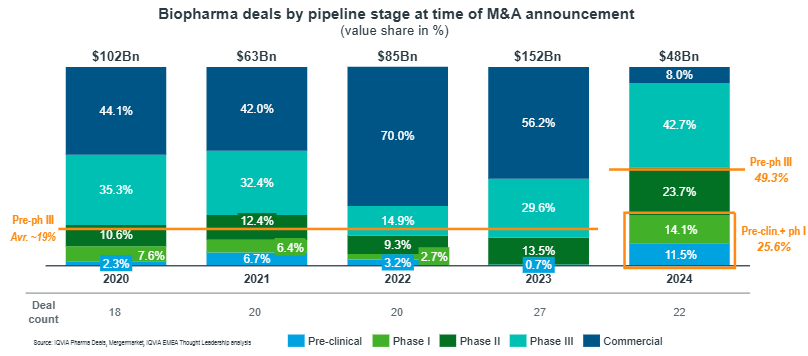

The media and the market may gravitate toward billion-dollar deals (like AZ acquiring EsoBiotech and Fusion Pharma), but some Biotech acquirers are quietly targeting companies in the sub-$500M space, seeking firms with strong data and a clean regulatory path (EY article on 2025 M&A Growth Strategy). The average BioPharma deal size fell from $5.6B in 2023 to $2.1B in 2024—in fairness, the federal funds rate was at its highest point since April 2007 and stayed through Sep 2024.

Biopharma M&A: Outlook for 2025 – IQVIA

Why it matters:

A company doesn’t need a unicorn valuation to get acquired. In fact, it’s often easier—and wiser—to buy a company with focused timelines and clean operating structures. Larger or older firms may carry legal disputes, bloated teams, or entangled partnerships that limit flexibility—the recurring costs of servicing these liabilities can erode the cash-flow projected during due diligence.

Who did it right: Abbvie’s $200M acquisition of Landos Biopharma in May 2024.

Landos Biopharma’s Specialty: Novel, oral therapies to treat autoimmune diseases. This acquisition added NX-13 (first-in-class asset to treat IBD) to Abbvie’s pipeline. NX-13 was developed using LANCE, a proprietary AI-based platform to identify novel oral therapies for autoimmune and inflammatory diseases.

Other examples: AbbVie’s acquisition of Celsius Therapeutics, Merck’s purchase of Abceutics, GSK’s acquisition of Elsie Biotech (all in 2024).

Finally, as capital becomes scarce, investors become more selective, and the market values execution over hype. For those driving biotech deal-making, recognizing these shifts is not just helpful—it’s a competitive advantage.